Kalshi faces backlash over Khamenei prediction market settlement

Users accuse the company of ambiguous contract terms after exchange resolves market at cents on the dollar

Prediction market operator Kalshi is facing significant user backlash and threats of a class-action lawsuit following the settlement of a high-volume market tied to the status of Iran’s Supreme Leader, Ali Khamenei.

At the center of the dispute is whether death constitutes “leaving a job” under the terms of the wager.

Kalshi says it does not. Traders argue that interpretation was not prominently disclosed.

The dispute is raising questions about transparency and governance at the federally regulated exchange.

Market Dynamics and User Expectations

The “event contract,” titled “Ali Khamenei out as Supreme Leader?” allowed users to bet on whether Khamenei would leave his position by a specified date. Because Iran’s Supreme Leader holds a lifetime appointment, many traders considered death the primary or only realistic mechanism for him to leave office.

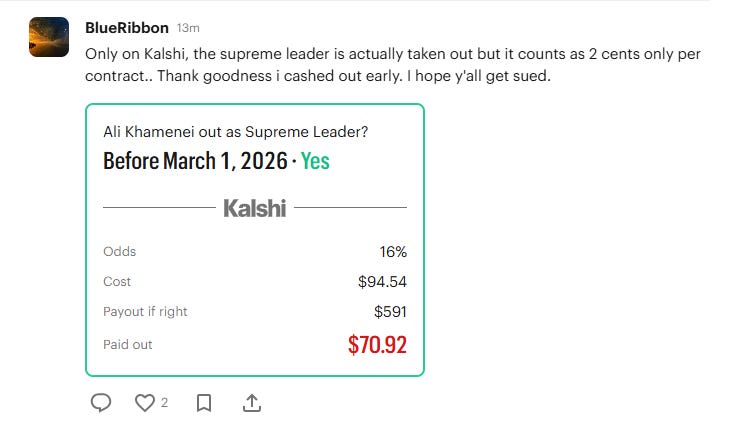

When rumors of Khamenei’s death circulated, Kalshi suspended trading. Instead of a full win for "Yes,” the exchange settled positions at the "last-traded fair price" before news of his death.

For traders holding “Yes” shares, that price was only a few cents on the dollar — a fraction of the $1 payout they had anticipated.

Rival prediction platform Polymarket, which is not federally regulated in the U.S., kept its corresponding market open. As news was confirmed, “Yes” shares climbed, and a full payout was delivered to holders. Traders who held "Yes" positions received their full expected payouts.

Traders critical of Kalshi argue that by freezing the market early, the company interfered with price discovery. That’s the process by which markets incorporate new information into asset prices. Some allege the move shielded “No” bettors from losses at the expense of “Yes” bettors.

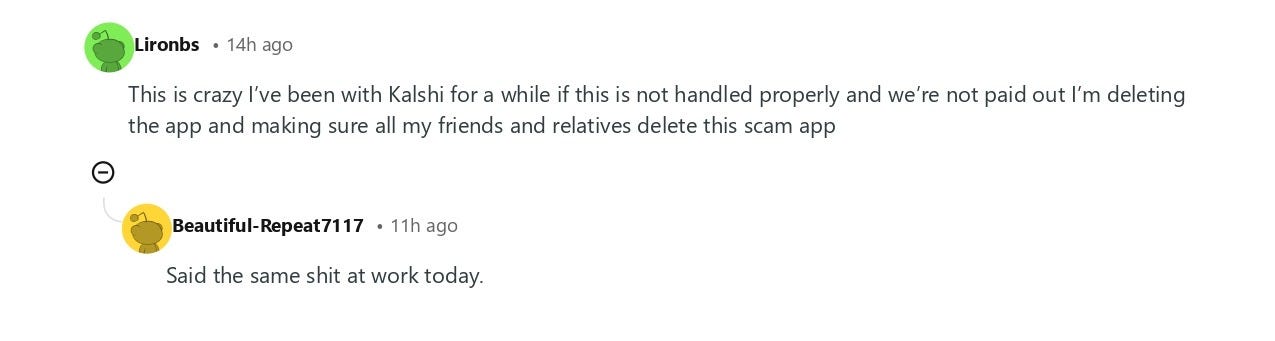

Traders on the Kalshi platform immediately began reacting to the situation in the exchange’s “prediction” post forum.

The “Death Carveout”

Kalshi maintains it followed its published rulebook. It says contracts include a “death carveout” provision stating that if a subject dies, the market resolves at the “last-traded fair price” rather than a “Yes” or “No” win.

As a U.S.-regulated exchange, Kalshi is overseen by the U.S. Commodity Futures Trading Commission (CFTC), which widely prohibits contracts that allow people to profit directly from a death.

Kalshi asserts its rules always specified that in the event of death, the market would resolve to the last traded price, not a full payout, to comply with these rules.

Users counter that the clause was not prominently communicated and that the market’s framing as a political status event implied death would qualify as being “out” of office. On the subreddit r/Kalshi, some users are now accusing the company of a “massive scam,” threatening a class-action lawsuit, and promising to delete the app over a lack of transparency.

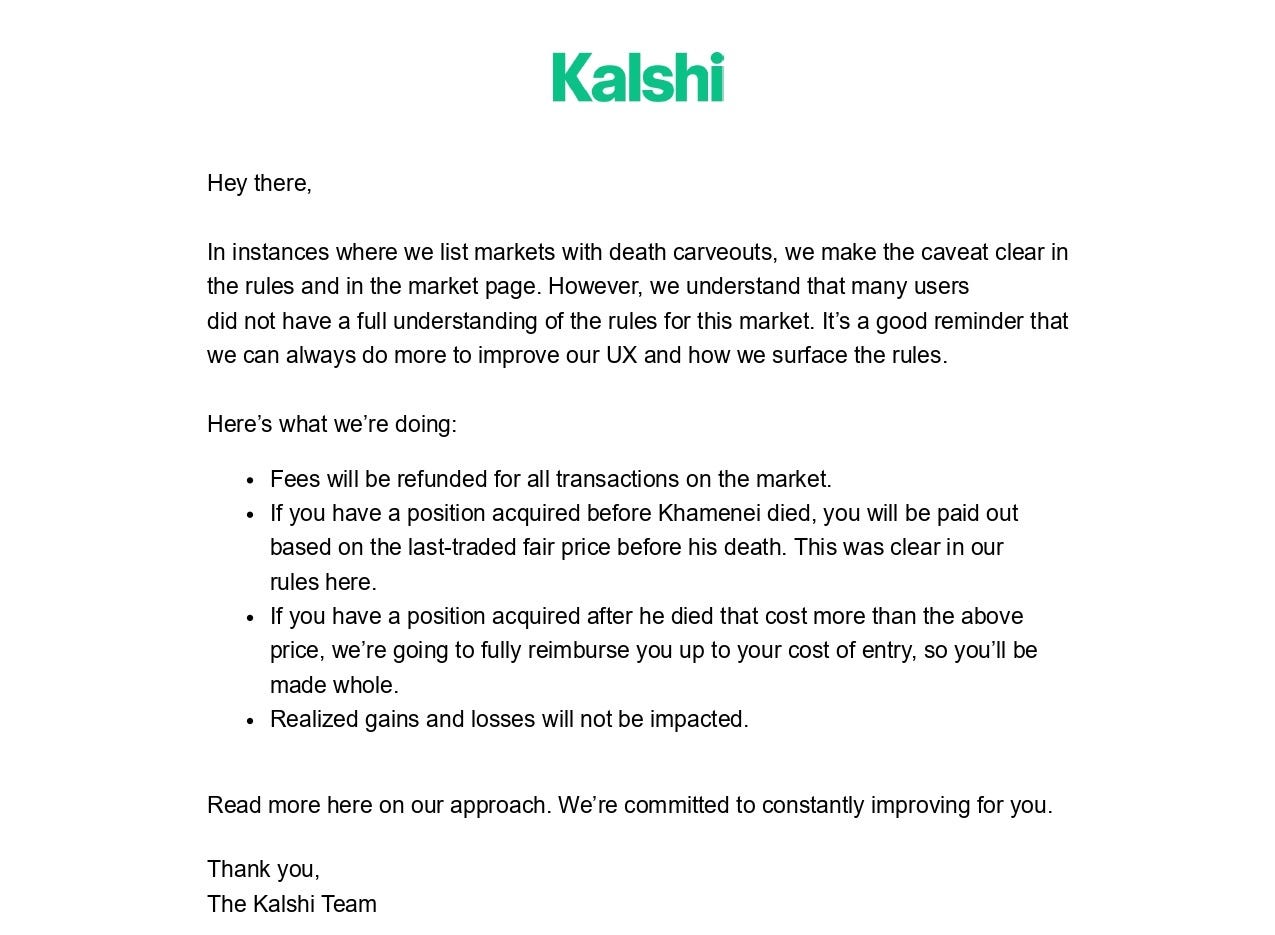

Kalshi’s Resolution Plan

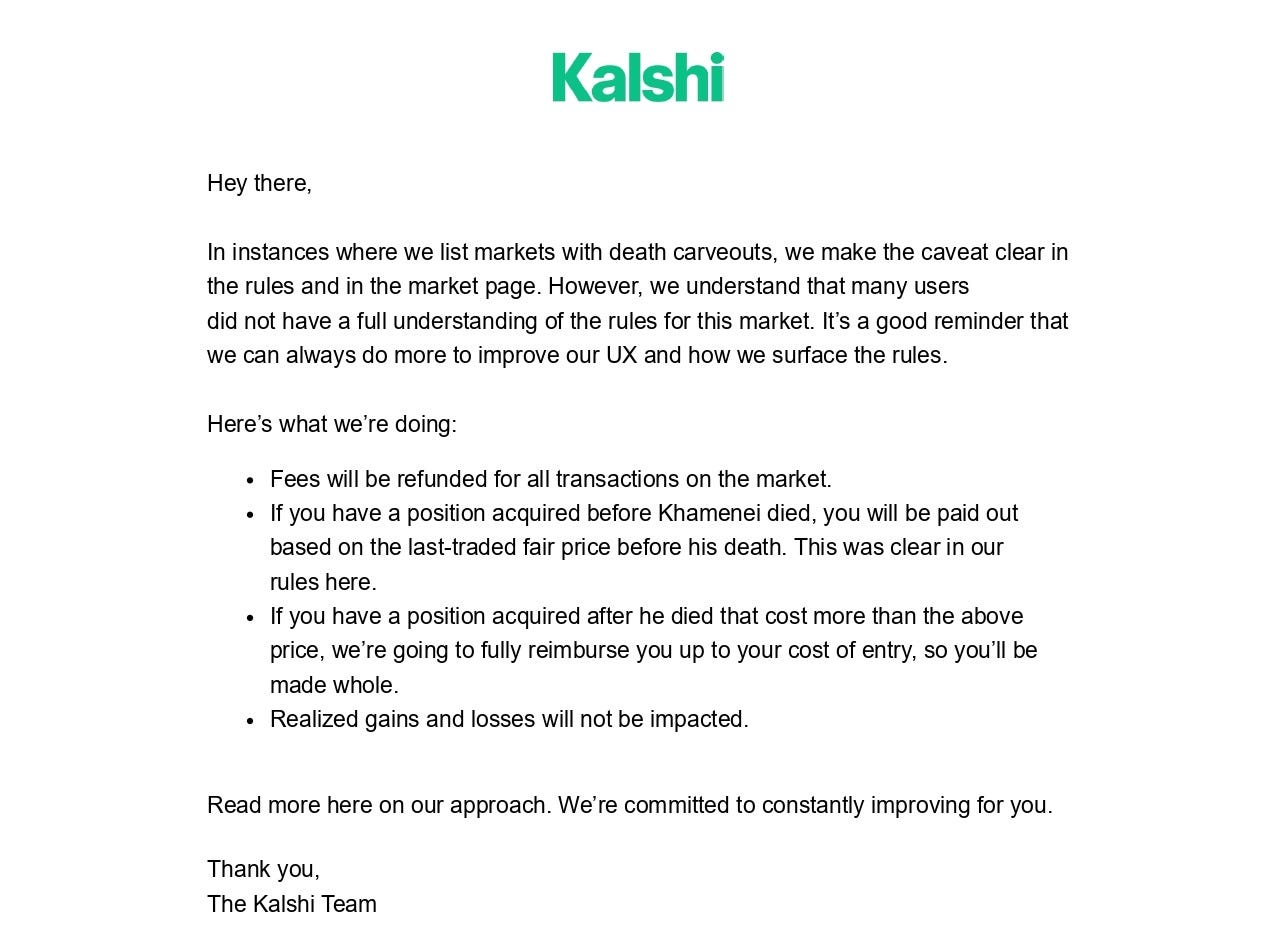

In an email to users, Kalshi acknowledged that there was “grammatical ambiguity” in the contract language and said it would improve how key rules are surfaced in the user interface.

The following is outlined in the exchange’s resolution plan:

All transaction fees will be refunded

Positions acquired before Khamenei’s death will be paid based on the last-traded price prior to his passing

Positions acquired after his death will be reimbursed up to the original cost of entry

Realized gains and losses will not be affected

Kalshi email to users | 28 Feb 2026

Political Optics and Broader Implications

The dispute lands at a time when prediction markets are facing growing scrutiny in the U.S.

Kalshi’s board includes Donald Trump Jr., a high-profile political figure whose connection to the dispute has amplified online backlash. While there is no indication he was involved in the market’s design or settlement, his affiliation has fueled perceptions among some online traders that politically sensitive event contracts risk becoming flashpoints in America’s broader culture wars over gambling, regulation and the monetization of real-world events.

The incident could prompt regulators to scrutinize how such contingency clauses are presented to traders. It also could test public trust in exchanges as event contracts expand into politics and geopolitics.

All in all, the controversy has exposed the friction between innovative market design and compliance boundaries for companies regulated by U.S. law.

Disclaimer: This information is for educational purposes and does not constitute legal or financial advice.